The Slovak government has introduced a tax amnesty through a regulation effective from 1 October 2025. The tax amnesty provides a temporary opportunity for individuals or companies to retroactively declare and pay taxes that they have not paid in the past, without penalties, interest or other criminal sanctions.

The tax amnesty applies to penalties and interest on arrears for all taxes, with the exception of local taxes and fees. It also does not apply to special levies, solidarity contributions, tax advances, taxes paid in instalments or tax deferrals. The tax amnesty also does not apply to tax arrears resulting from tax audits.

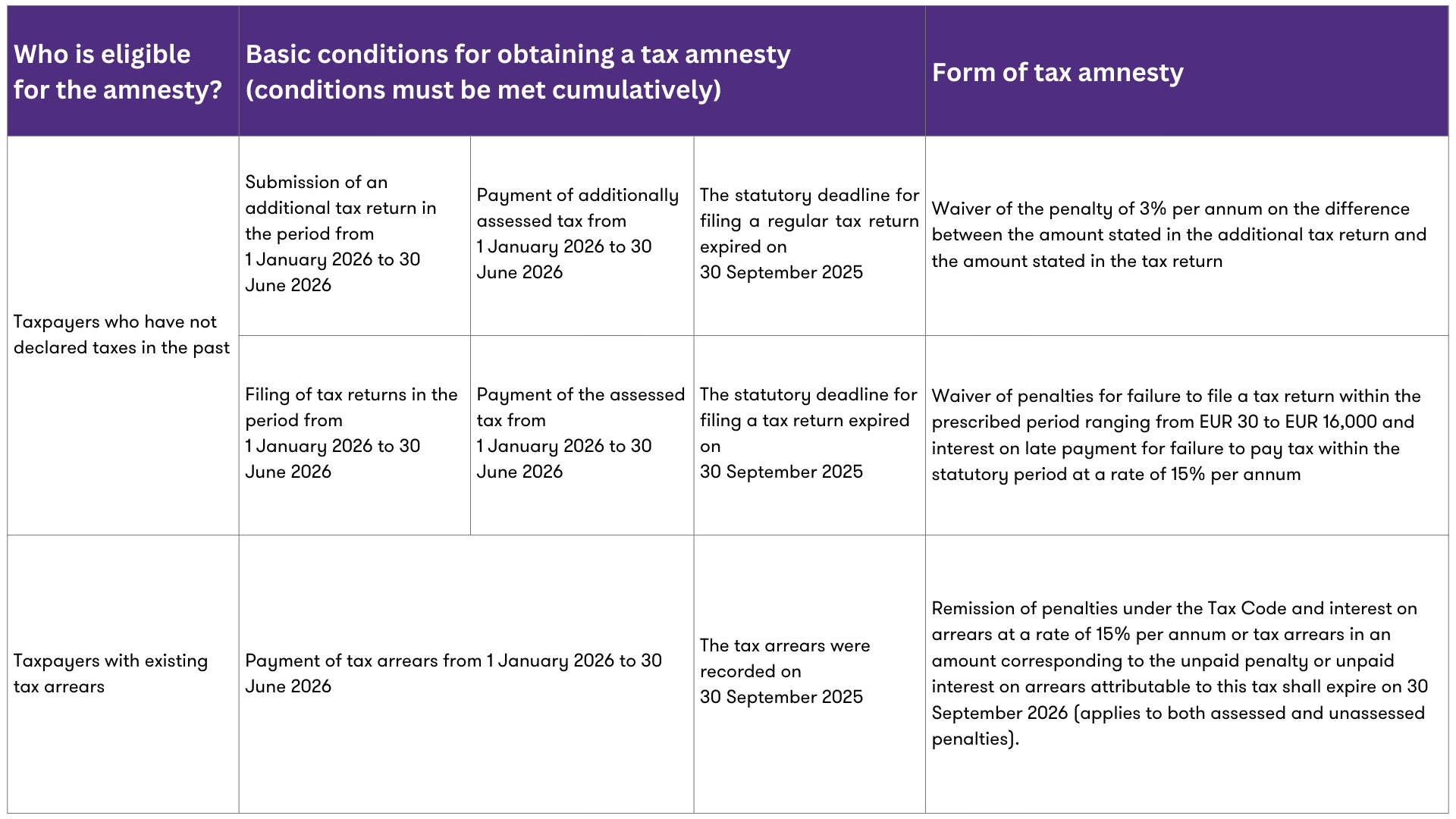

The following table provides a brief overview of the conditions for applying the tax amnesty:

Table: Brief overview of the tax amnesty – who it applies to, basic conditions, and types of forms

Practical examples

Example no. 1

As of 30 September 2025, the company has a tax arrears on income tax in the amount of €1,000. If the tax administrator proceeded in the standard manner, it would impose a fine of €200 on the company pursuant to Section 155 of the Tax Code and penalty interest for late payment of €150 pursuant to Section 156 of the Tax Code. However, since the taxpayer pays the basic debt in full, €1,000, on 10 March 2026, the state will not impose any penalty or interest under the tax amnesty. The company will pay only €1,000, without any additional penalties.

Example no. 2

As of 30 September 2025, the company has an income tax arrears of €1,000. In addition, it already has a legally imposed but unpaid penalty of €200 and interest on arrears of €80. The company pays the entire tax arrears of €1,000 on 15 March 2026. The remaining arrears on the penalty and interest will expire by law on 30 September 2026.

Example no. 3

An entrepreneur was required to file an income tax return for 2024 by the end of March 2025 at the latest, but failed to do so. He files his return almost a year late on 12 February 2026 and pays the calculated tax liability of €1,000 on 18 February 2026. Thanks to the tax amnesty, the tax administrator will not impose a penalty for late filing of the tax return or charge interest on arrears. The taxpayer will only pay the net income tax amount of €1,000.

Example no. 4

A VAT payer filed a proper return for the March 2025 tax period, claiming an excess deduction of €7,000. He later discovered an error and filed an additional tax return on 4 February 2026, adjusting the excess deduction to the correct amount of €4,500. He paid the resulting difference of €2,500 to the State Treasury on 5 February 2026. In this case, the tax administrator will not impose a penalty that would otherwise result from the filing of an additional return.

Example no. 5

The company filed a notification for the new financial transaction tax for August 2025 by the regular deadline of 30 September 2025, but did not pay the tax itself on that date. In this case, the tax amnesty does not apply because the tax arrears arose on the day after the due date, 1 October 2025. The amnesty applies only to arrears that existed on or before 30 September 2025, not to those that arose after that date.

Example no. 6

A tax audit of the company's corporate income tax for the 2023 tax period was opened and completed in January 2026 with additional tax assessed. In this case, the tax amnesty does not apply to the taxpayer, and additional tax and a penalty will be assessed.

Finally, we note that tax amnesty is a form of state aid. If the taxpayer has exceeded the de minimis state aid threshold, they are not eligible for tax amnesty.