Branislav Mačuha | 17.4.2026 | News

Starting January 1, 2027, businesses will face a significant change in invoicing: the introduction of mandatory electronic invoicing and digital data reporting to the Slovak Financial Administration. This change replaces the current practice of sending invoices in paper forms or as standard PDF files, which in some cases will no longer be sufficient to meet legal requirements.

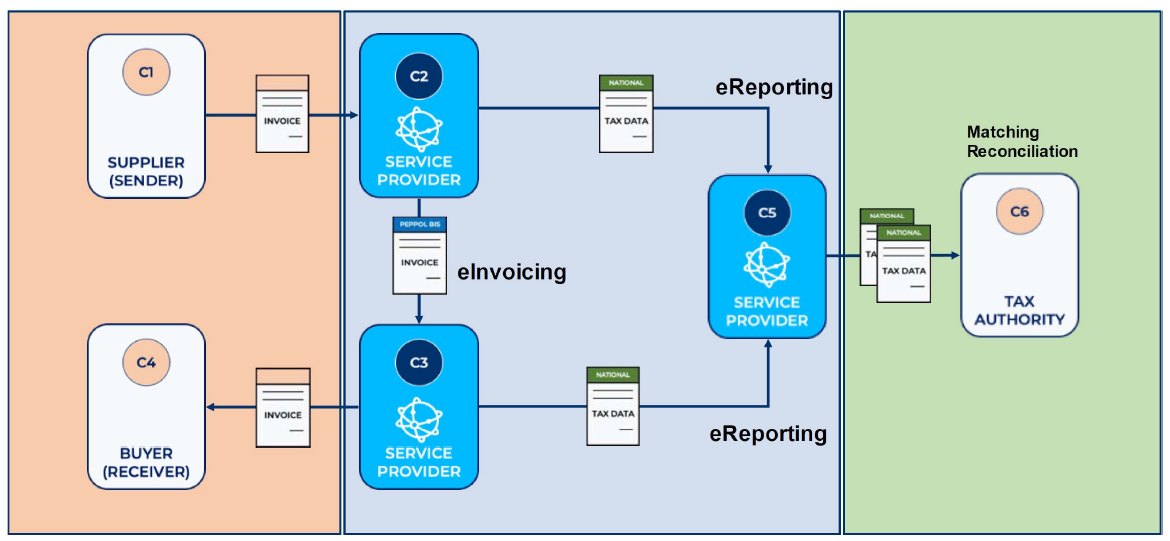

Most businesses today use invoices in PDF format, which is, however, only an “image” without structured data. The new system requires that invoices will be issued in a standardized XML format in accordance with an European standard. It is assumed that computer systems will be able to automatically read and process data from e-invoices without any need of manual transcription, thereby eliminating errors and speeding up administrative processes. The new regulation establishes precise rules for the creation, sending, and receiving of e-invoices through certified service providers.. The list of certified service providers is published on the Financial Administration’s website. They are commercial entities certified by the Financial Administration that will provide this service of sending and receiving e-invoices for a fee. The fee amount is not regulated by state authorities.

The obligation to issue e-invoices will apply to all VAT payers established in Slovakia who will supply goods or services in Slovakia to a domestic taxable person or a domestic non-taxable legal entity. At the same time, the obligation to accept such an electronic invoice applies to every entity to which the issuer is required to issue an e-invoice, regardless of whether the recipient is a VAT payer or not. Certified service providers will therefore be used not only by all businesses with their registered office or place of business in Slovakia but also by the nonprofit sector, municipalities, and other legal entities based in Slovakia, regardless of whether they are registered for VAT purposes.

VAT payers will be also required to report e-invoice data to the Financial Directorate of the Slovak Republic. The advantage of this system is that reporting should generally be automated through the certified services providers the businesses contracted with. However, if the data is not reported, the businesses themselves face high penalties.

From beginning of June 2026, it should be possible to use the system on a voluntary basis. The Financial Administration recommends using this period for preparation—particularly for selecting a suitable certified service provider or verifying whether your accounting software will be prepared for electronic invoicing via the Peppol network.

Accounting software providers can become certified service providers directly or act solely as intermediaries between businesses and the certified service providers. It is expected that various applications or websites that are not directly connected to accounting software will likely also be available on the market, which can be used primarily by smaller companies or companies that have software without the direct capability to issue electronic invoices.

These changes will also reduce the administrative burden in the future. Starting July 1, 2030, the obligation to issue e-invoices will be extended to cross-border transactions throughout the European Union, which is why there are plans to eliminate the requirement to file EC sales lists. It is also expected that the scope of transactions reported in the control statement will be significantly reduced, with only transactions not subject to e-invoicing—such as the purchase of services from third countries. For a certain period, however, both systems will operate concurrently, which will result in a temporary increase in the administrative burden.

For transactions with a third country, the delivery of a new means of transport by a person other than the VAT payer, and in the case of distance sales of goods to another EU Member State where the supplier applies a special scheme, it is not necessary to issue an e-invoice. A standard invoice, in paper or pdf form is sufficient.

When supplying goods or services to the Slovak Information Service, Military Intelligence, or if the supply is related to classified information, requires classified information, or contains classified information, an e-invoice must not be issued.

The minimum legal requirements for an e-invoice are:

In addition to legal requirements, certified service providers and accounting software developers must also take into account PEPPOL BIS conditions in the Slovak Republic, which, beyond the scope of the Slovak VAT act, defines which data on an e-invoice is mandatory and essential for the successful transmission of the e-invoice via a certified service provider — if the invoice does not contain all the required elements, PEPPOL network will automatically reject the invoice (in addition to the legal requirements, this includes, for example, the invoice type code, due date, and others).

The e-invoice must be issued within 15 days:

Credit and debit notes must also include the serial number of the original e-invoice and data that are amended. Credit or debit notes must be issued within 15 days from the end of the calendar month in which the reason for the adjustment of the tax base occurred.

A summary e-invoice may be issued for multiple separate supplies of goods or services or for multiple payments received before the supplies, covering a maximum period of one calendar month. The summary e-invoice must be issued within 15 days after the end of the calendar month.

The e-invoice must be issued, sent, and received in an electronic document format that allows its automated and electronic processing (in practice, XML format), and in a data structure compliant with the technical standard for electronic invoicing EN 16931—in practice, this is the Peppol BIS 3.0 format. Compliance is typically ensured by the certified service provider.

E-invoices must be retained for a period of ten years from the end of the calendar year to which the electronic invoices relate.

As of July 1, 2030, the deadline for issuing the e-invoice will be reduced to 10 days.

(applies only to e-invoices sent via certified service providers, not by the other method)

The supplier reports e-invoice data to the Financial Directorate via their certified service provider within five days after the date the e-invoice was issued or from the date the deadline for issuing the e-invoice expired (if the electronic invoice is issued by the customer in the name and on behalf of the supplier).

The customer shall report the e-invoice data to the Financial Directorate via their certified service provider within five days after the date of e-invoice receipt only if the customer is a VAT payer.

Data to be reported to the Financial Directorate:

Up to EUR 10,000 for failure to report, incomplete reporting, incorrect reporting, or late reporting of e-invoice data to the Financial Directorate. For repeated violations, a fine of up to EUR 100,000 may be imposed. Penalties are imposed directly to the taxpayer, not the certified service provider.

The reporting obligation is considered fulfilled upon delivery of the electronic invoice to the certified service provider.

The penalty will not be imposed if:

The possibility to voluntarily test electronic invoicing in a “live” environment is expected in June 2026 or at the beginning of June 2026. However, the recipient’s consent is required, unless the recipient has confirmed that they can receive electronic invoices via the certified service provider. The first step is to check with your accounting software provider if their solution will not only be able to issue e-invoices, but also to receive e-invoices: if not, consider how you will issue and receive electronic invoices, whether through an external service provider outside the accounting software environment with a potential automated connection to your accounting software, or whether you consider a change to another accounting software that already has an e-invoicing solution directly built in. In accordance with Peppol rules, companies may have only one certified service provider for receiving documents. On the sending side, however, companies can test multiple service providers simultaneously and later choose the one that suits them best. We highly recommend using the testing period until the end of 2026 to set up and try e-invoice processes with a selected sample of suppliers and customers, so that you’ll be ready to receive and issue invoices electronically starting in January 2027.

Currently, a demo of the accounting software, a demo of the e-invoice creation application, an e-invoice validator demo, demo of peppolbox and an informational website about e-invoices are also available. Please note that websites are for education purposes only – real e-invoices cannot be sent and received via them.

Verner Hakoš | 16.7.2026 | News

The tax authorities may automatically register several…From 1 January 2026, the tax authority may, by virtue of its official powers,…

Filip Tichý | 30.6.2026 | News

Global intent, local reality: What does sustainability…Sustainability is a shared ambition at a global level, yet the way it is…

Jana Kyselová | 26.6.2026 | News

How to correctly include foreign dividends in your personal…Anyone who invested in foreign shares or mutual funds last year could extend…