Verner Hakoš | 13.4.2026 | News

On January 1, 2026, three significant amendments to Tax Code No. 563/2009 Coll. (Tax Code) will take effect. In addition to several technical legislative adjustments, they also introduce significant increases in penalties that will affect a wide range of taxpayers.

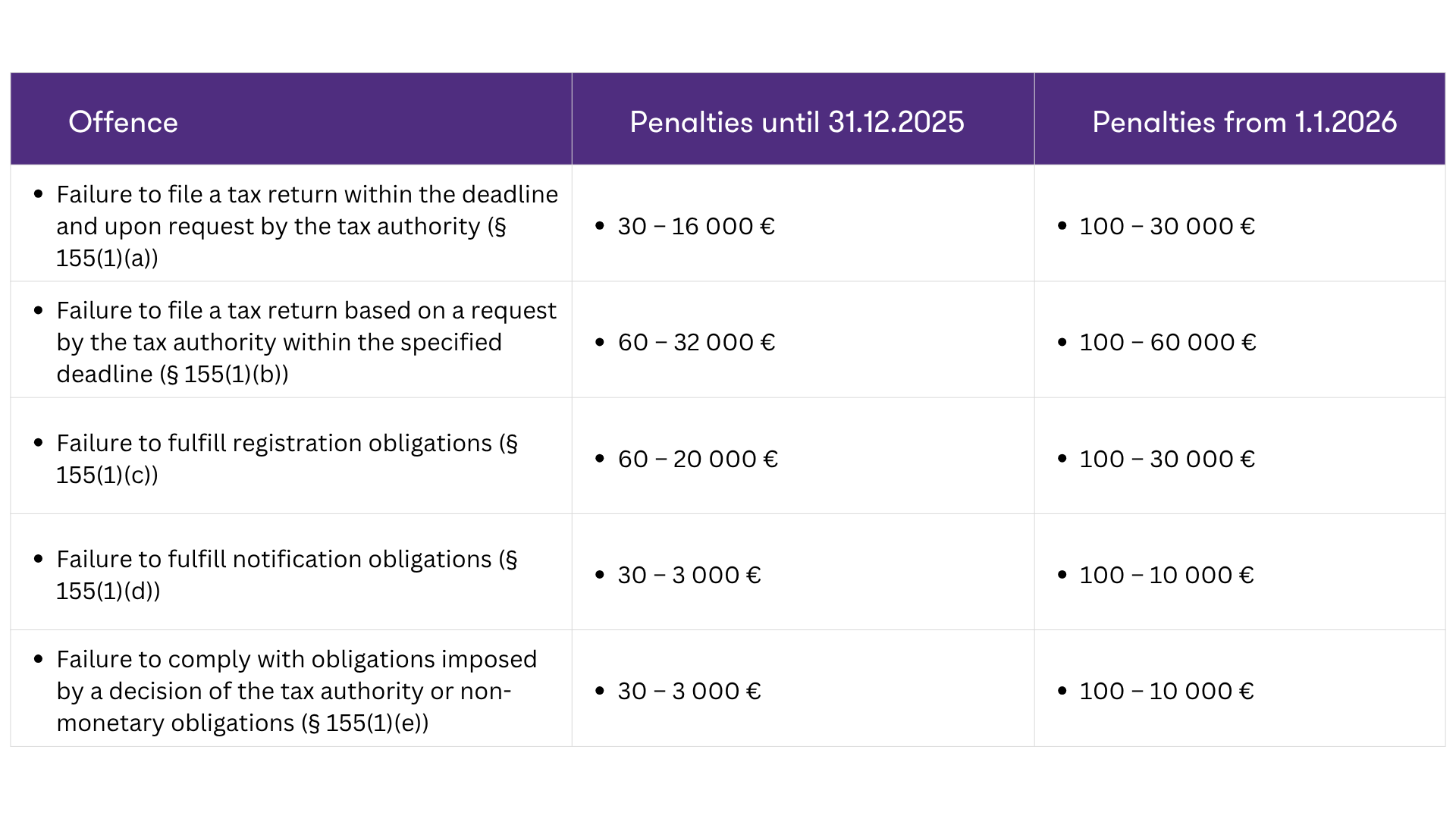

The new legislation significantly raises both the minimum and maximum limits of fines for violations of tax obligations. At the same time, however, it introduces an incentive mechanism inspired by the system of traffic penalties, in the form of a reduction in the fine if paid on time.

The key change concerns an increase in rates for the following offenses:

These changes will apply to violations occurring after December 31, 2025. When imposing fines, as before, the tax administrator will take into account the duration and severity of the violation. Furthermore, when imposing a fine at the upper limit, the tax administrator will be required to properly justify their decision.

The amendment adds a new paragraph 17 to Section 155, introducing an incentive mechanism for taxpayers. If a taxpayer pays the assessed tax, tax difference, or improperly claimed amount within 15 days of receiving the decision, the fine will be reduced to two-thirds.

However, this mechanism applies only to penalties determined as a percentage (e.g., of the tax difference), not to the penalties mentioned above, where the sanctions were increased. Upon timely payment, the taxpayer does not lose the right to seek remedies; that is, the right to file an appeal remains intact.

From an implementation perspective, the process will proceed as follows: the tax administrator will initially issue a decision with the penalty amount already reduced (i.e., to two-thirds). In the event of non-payment within the specified period, a new decision will subsequently be issued for the full amount of the penalty. This procedure differs from the model used for traffic fines, which served as its inspiration.

Furthermore, the amendment also introduced several procedural changes:

According to statements by the Financial Administration, the aim of the legislative changes is to strengthen the disciplined fulfillment of tax obligations, increase the preventive effect of penalties, and motivate taxpayers to promptly pay assessed liabilities.

The amendment provides room for mitigating penalties in the event of a prompt response by taxpayers. For honest business owners, nothing fundamentally changes; as before, the key for them will remain the proper setup of internal processes and monitoring of deadlines. For other types of business owners, this change will serve as a deterrent in the form of higher penalties; however, only time will tell if it will be effective, as the Financial Administration anticipates.

Verner Hakoš | 16.7.2026 | News

The tax authorities may automatically register several…From 1 January 2026, the tax authority may, by virtue of its official powers,…

Filip Tichý | 30.6.2026 | News

Global intent, local reality: What does sustainability…Sustainability is a shared ambition at a global level, yet the way it is…

Jana Kyselová | 26.6.2026 | News

How to correctly include foreign dividends in your personal…Anyone who invested in foreign shares or mutual funds last year could extend…

Ľubomíra Murgašová | 19.6.2026 | News

From 1 July, you will pay a new fee for parcels from China,…From 1 July 2026, a major change to the European Union’s customs rules will…