Jana Kyselová | 26.6.2026 | News

Anyone who invested in foreign shares or mutual funds last year could extend the deadline for filing their tax return to 30 June or 30 September 2026. This is a logical step, as obtaining the necessary certificates and supporting documents from abroad can take longer than for domestic investments.

If a natural person – a tax resident in the Slovak Republic – had this type of income for the year 2025 but forgot to include it in their tax return by the deadline of the end of March 2026, they should file their tax return for 2025 without delay. When including investment income in a tax return, it is essential not to overlook the taxation of .

This is because the tax authority can identify this type of income through the international exchange of information that takes place between foreign banks and tax authorities. From January 2026, a fine of between EUR 100 and EUR 30,000 may be imposed for filing a tax return after the statutory deadline. No fine is imposed for filing an amended tax return.

If the tax return results in an additional tax liability, the tax administrator is entitled to impose:

Given that investing in securities is more popular today than ever before – mainly thanks to digital platforms, mobile apps and growing financial literacy among ordinary people – the obligation to declare business income in tax returns applies to a large proportion of Slovaks. According to estimates, up to 30% of Slovaks invest in some form on the financial markets.

A common form of foreign income from investment is the dividend paid to an investor (a natural person) for holding purchased foreign shares over a certain period. In practice, however, we also see dividends arising from participation employee stock ownership programs at foreign companies – typically at the parent company.

In practice, most countries deduct tax from dividends at the time of payment to the investor. This means that this income is not subject to withholding tax in Slovakia at the time of payment, as is the case with dividends from Slovak companies.

In practice, however, there is a misconception that if dividends have already been taxed abroad, they do not need to be included in the tax return. A tax resident in the Slovak Republic must, however, declare dividend income at home as well.

To avoid double taxation of this income (abroad vs. Slovakia), two main methods are used – the credit method and the exemption method. Which one is used depends on the specific Double Taxation Agreement between the Slovak Republic and the country from which the dividends originate.

The tax credit method is most commonly applied in the context of the personal income tax return – Type B:

If the tax withheld abroad is higher than the tax rate under the Double Taxation Agreement between Slovakia and the relevant country (DTA), a Slovak tax resident may apply for a tax refund directly in the country where the dividends were taxed. A tax refund can be requested directly from the relevant foreign tax authority by submitting a completed form available on the foreign tax authority’s website, or through Slovak companies specialising in tax refunds from abroad.

|

Tax rate |

Country |

|

15% |

USA |

|

10% |

Austria |

|

15% |

Germany |

|

10% |

Taiwan |

Any tax resident of the Slovak Republic who receives dividends from a foreign company must declare them in their personal income tax return (Type B), even if they have already been taxed abroad.

The income tax rate depends on the accounting period in which the profit was generated:

In total, a natural person completes the following sections of the tax return:

In 2025, a natural person received dividends from the profits of 2024 paid out by foreign companies.

Overview of dividends and withholding taxes

|

Dividend amount |

Country of source |

Withholding tax deducted in the source country |

Applicable tax rate under the DTA |

Amount of withholding tax under the DTA recognised for credit against Slovak tax |

Amount of Slovak tax (10%) |

|

EUR 600 |

Austria |

EUR 165 |

10% |

EUR 60 |

EUR 60 |

|

EUR 300 |

USA |

EUR 45 |

15% |

EUR |

EUR 30 |

|

EUR 900 |

x |

EUR 210 |

x |

EUR 105 |

EUR 90 |

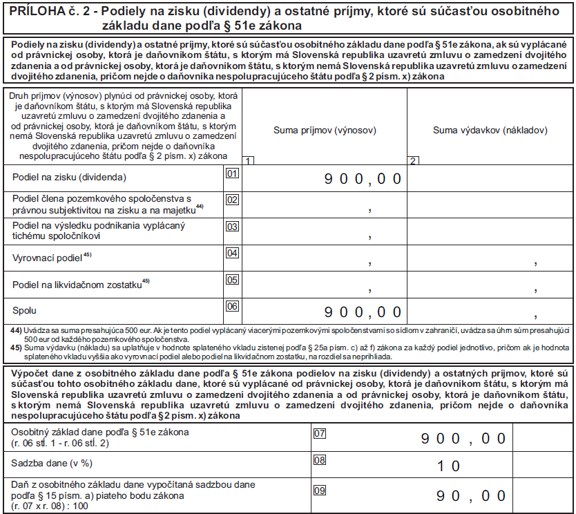

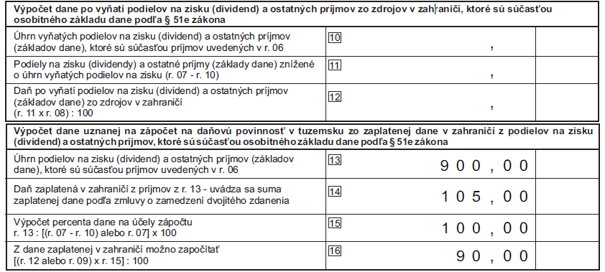

The amount of dividends received is stated in Appendix 2, which forms part of the tax return.

The following lines must be completed in this Annex (the remaining lines will be calculated automatically):

Line 01 – enter the total amount of dividends received.

Line 08 – enter the Slovak tax rate.

Line 13 – enter the amount of dividends received again here.

Line 14 – enter here the amount of withholding tax calculated using the tax rate specified in the relevant DTA.

From the example above, we can see that after offsetting the tax withheld abroad against the Slovak tax, the individual did not incur any additional tax liability. Therefore, no amount is entered in line 18.

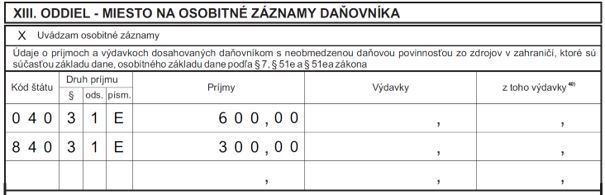

To ensure the tax return is completed correctly, information on dividends received must also be included in the Special Entries section of the tax return in the following format:

Ľubomíra Murgašová | 19.6.2026 | News

From 1 July, you will pay a new fee for parcels from China,…From 1 July 2026, a major change to the European Union’s customs rules will…

5.6.2026 | News

President Zuzana Čaputová at Grant Thornton: I Wish All of…On Thursday, May 21, we welcomed clients, employees, and friends of the firm to…

Martina Švaňová | 25.5.2026 | News

Pay Transparency: What the New Law Will Bring from June 2026A new era of pay transparency in Slovakia begins on 7 June 2026. On 15 April…